The blind box economy has sparked a craze in the consumer market in recent years. As a leading player in this sector, Pop Mart's business expansion and the explosive popularity of its IPs have drawn significant attention. At the 2025 Yongle Spring Auction, a globally exclusive mint-colored LABUBU sold for 1.08 million yuan. This price not only set a new record for a single collectible toy but also elevated Pop Mart's market influence to unprecedented heights. With blind boxes as its core product, Pop Mart has built a complete commercial ecosystem spanning design, production, and sales.

This “surprise-box” consumption model precisely taps into the emotional needs of young consumers, propelling the company to become Hong Kong's “first stock in the trendy toy sector” (09992.HK). By June 2025, its market capitalization surpassed HK$300 billion. Founder Wang Ning, with a net worth of US$20.3 billion, overtook Qin Yinglin of Muyuan Foodstuff to become Henan's wealthiest individual, demonstrating the wealth-creating power of the trendy toy economy.

However, as the blind box business model gained widespread popularity, controversies surrounding its potential “gambling attributes” continued to intensify. This article will conduct an in-depth analysis of the gambling-related risk factors inherent in the blind box economy's operational logic, offering a multi-dimensional perspective to clarify the industry's regulatory boundaries.

PART 1

PART 1

Pop Mart's Blind Box Business Model

The core of Pop Mart's success lies in its unique and highly appealing business model, with the blind box sales approach serving as a pivotal element.

The surprise consumption chain triggered by probability mechanisms. When purchasing blind boxes, consumers cannot predict the specific product inside. This uncertainty, akin to a lottery, greatly stimulates curiosity and the desire to explore. Each opening of a blind box feels like embarking on an unknown adventure—you might get a common item, or luckily draw a rare hidden variant. This instant thrill or disappointment drives consumers to keep trying, chasing that unexpected delight. For example, the probability of obtaining a hidden variant in Pop Mart's Molly series, SKULLPANDA, or DIMOO series is 1 in 144, approximately 0.694%. This extremely low probability makes securing a hidden variant a highly rewarding achievement, compelling consumers to make repeated purchases.

PART 2

PART 2

The Gambling Risks Behind the Explosive Blind Box Economy

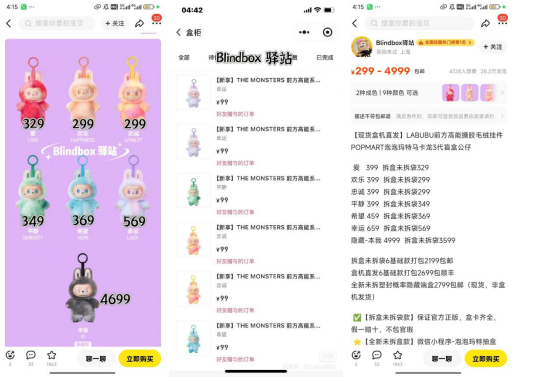

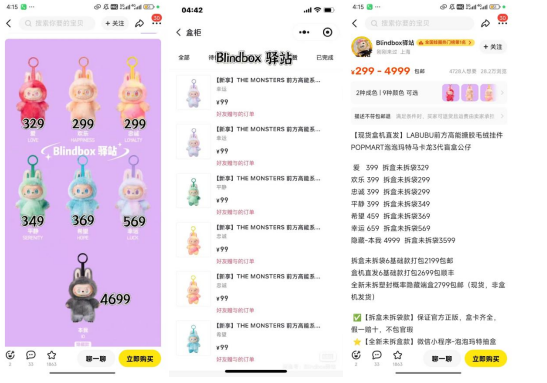

The hidden editions of Pop Mart blind boxes command significant premiums in the secondary market due to their scarcity. This lucrative effect not only drives consumers to make frequent repeat purchases but also fuels large-scale arbitrage reselling on platforms like Xianyu. When brands become deeply entangled with secondary market transactions, they risk crossing legal boundaries, potentially falling into the controversial realm of gambling activities or even operating gambling establishments. Below, we analyze the legal risks behind blind boxes from a scenario perspective:

Scenario 1: Official Direct Buyback of Blind Boxes

Scenario 1: Official Direct Buyback of Blind Boxes

If a brand implements a direct buyback mechanism for blind boxes—particularly by offering premium buybacks for rare variants—it constitutes a classic gambling-related legal risk. In traditional gambling, participants invest money hoping to gain higher returns through uncertain outcomes.

When the official entity directly repurchases, consumers' purchase of blind boxes resembles placing bets in gambling, while the official repurchase functions like the prize redemption phase. Consumers invest a certain amount when purchasing blind boxes. If they obtain a rare item, the official entity repurchases it at a high price. This allows consumers to gain monetary benefits from this uncertainty, fully aligning with gambling's characteristic sequence of “investment - uncertain outcome - profit acquisition.”

Consider the “A8 Sports” gambling case [Case No.: (2019) Yue 03 Xing Zhong 2614]. The platform's probability-based betting games bore striking similarities to blind box mechanics: users paid to bet, winning virtual tokens redeemable for JD E-cards. A8 officials facilitated cash-out loops by arranging for money dealers to repurchase these JD E-cards from gamblers within official WeChat groups. Ultimately, the platform's officials were convicted of operating a gambling establishment. This precedent clearly establishes that when commercial activities employ “official buybacks” to transform uncertain commodity acquisition into monetary profit chains, they are highly susceptible to being classified as gambling.

Scenario 2: Official Buybacks via Agents/Third Parties

Even when officials do not conduct buybacks directly but instead utilize agents or third parties, the essence remains largely unchanged. As long as a connection or tacit understanding exists between officials and these intermediaries, making buybacks an open, consumer-recognized profit channel, gambling risks arise.

For example, if the official entity secretly colludes with a secondary trading platform that purchases rare blind boxes at inflated prices, and consumers knowingly buy blind boxes to resell them for substantial profits, they actively participate in purchasing. In this scenario, although the official entity appears not to be directly involved in repurchasing, it has effectively established a channel through a third party for converting blind box purchases into monetary gains, still constituting a gambling mechanism.

Scenario 3: Risks of Market Speculation Run Amok

Although Pop Mart officially claims non-involvement in the secondary market and refrains from intervening in price fluctuations, reality shows that blind boxes—especially rare ones—are inflated to astronomical prices on resale platforms. When high-priced resales proliferate in the secondary market and consumers purchase blind boxes with explicit expectations of profit through resale, blind box transactions risk evolving into gambling-like activities.

Objectively, some consumers purchase blind boxes not purely out of affection for collectibles, but as an investment strategy—hoping to profit by buying blind boxes and reselling rare items at inflated prices in the secondary market. This investment-driven purchasing behavior shifts blind box transactions beyond normal commodity sales, resembling speculative gambling where economic gains depend on unpredictable draw outcomes.

Take the “Wanwushang” platform gambling case [Case No.: (2025) Zhe 0727 Xing Chu 22] as an example. This platform used apps and WeChat mini-programs like “Wanwushang,” " Wish Blind Box" and other apps and WeChat mini-programs to establish a gambling system under the guise of selling blind boxes. Multiple defendants participated by providing currency exchange services for gamblers, ultimately being convicted of operating a gambling establishment.

PART 3

High-Priced Resale in Secondary Market Conflicts with Prize Promotion Regulations

China's Anti-Unfair Competition Law explicitly stipulates that prize promotions involving lottery-style sales with top prizes exceeding 50,000 yuan constitute unfair competition.

Although Pop Mart's official blind box sales do not qualify as lottery-style prize promotions, the phenomenon of reselling at inflated prices in the secondary market creates a situation where blind boxes undergo distribution processes resembling prize promotions—with prize values far exceeding the legal threshold. For instance, on the Xianyu platform, multiple Labubu blind boxes are being sold at prices significantly exceeding ¥50,000.

This phenomenon of high-priced resale, though not directly orchestrated by official entities, has formed a closed-loop cycle within the entire commercial chain: “purchase - open the box - resell for profit.” When consumers buy blind boxes, they have already incorporated the notion that “drawing a rare item = securing a substantial return” into their purchasing decisions. This transforms blind box transactions from simple commodity exchanges into speculative activities, further fostering a gambling-like consumer mentality where “buying blind boxes = buying lottery tickets.”

This phenomenon of high-priced resale, though not directly orchestrated by official entities, has formed a closed-loop cycle within the entire commercial chain: “purchase - open the box - resell for profit.” When consumers buy blind boxes, they have already incorporated the notion that “drawing a rare item = securing a substantial return” into their purchasing decisions. This transforms blind box transactions from simple commodity exchanges into speculative activities, further fostering a gambling-like consumer mentality where “buying blind boxes = buying lottery tickets.”

The high prices achieved in secondary markets are causally linked to the officially controlled rarity rates of collectible items. This dynamic entices consumers to invest excessive funds in blind boxes, hoping for substantial returns on the secondary market. Consequently, they fall into irrational consumption patterns, further amplifying the gambling-related risks within the blind box market.

PART 4

Final Thoughts

The explosive popularity of Pop Mart blind boxes reflects young consumers' enthusiasm for the “surprise economy,” yet the underlying gambling risks cannot be overlooked. Currently, China's regulation of the blind box economy remains in its exploratory phase, with relevant laws and regulations still incomplete.

Regulatory authorities must urgently clarify the compliance boundaries for blind box marketing, particularly guarding against the risk of “probability games” being distorted into gambling tools. Simultaneously, businesses must uphold social responsibility by avoiding the creation of speculative bubbles through scarcity tactics, rather than solely pursuing short-term profits.

For consumers, the essence of blind boxes should be “surprise,” not “speculation.” If market hype is left unchecked, blind boxes may ultimately become tools for exploiting unsuspecting buyers. Only when the market regains rationality and regulation steps in promptly can the blind box industry achieve sustainable development through a blend of creativity and commerce.

PART 1

PART 1 PART 2

PART 2 场景一:官方直接回购盲盒

场景一:官方直接回购盲盒 这种高价转售现象虽非官方直接参与,却在整个商业链条中形成了 "购买 - 抽盒 - 转售获利" 的闭环。消费者购买盲盒时,已将“抽中稀有款 = 获取高额回报”纳入消费决策,使得盲盒交易从单纯的商品买卖异化为投机行为,更催生了“买盲盒 = 买彩票”的赌博式消费心理。

这种高价转售现象虽非官方直接参与,却在整个商业链条中形成了 "购买 - 抽盒 - 转售获利" 的闭环。消费者购买盲盒时,已将“抽中稀有款 = 获取高额回报”纳入消费决策,使得盲盒交易从单纯的商品买卖异化为投机行为,更催生了“买盲盒 = 买彩票”的赌博式消费心理。