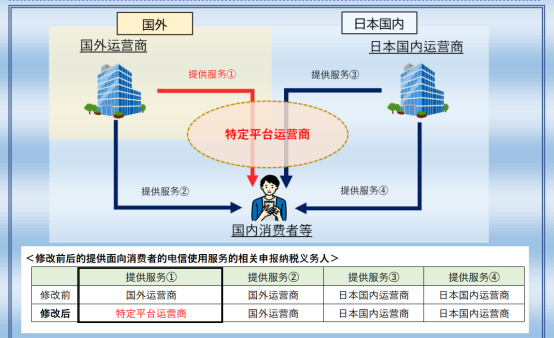

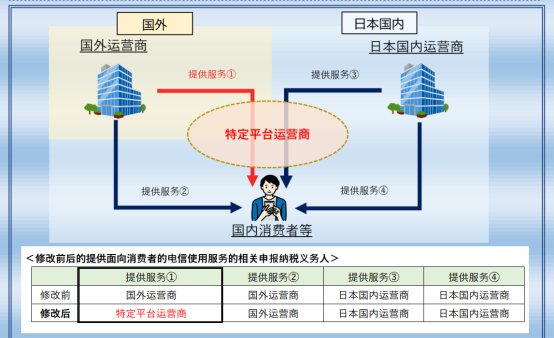

In February 2025, the Japanese government officially announced that it would collect a 10% consumption tax on behalf of non-Japanese developers starting April 1. Previously, Apple Inc. had been designated by Japanese tax authorities as a specific platform operator. It announced that effective April 1, 2025, all paid applications and in-app purchases (including game items) made by non-Japanese developers on the App Store would be subject to a 10% Japanese consumption tax, collected by Apple on their behalf.

In February 2025, Hong Kong-based game company Yota Games was ordered by Japan's Tokyo National Tax Agency to pay approximately ¥1.8 billion in back taxes for failing to remit consumption tax related to in-game item sales. Previously, Epic Games was also ordered by Japanese tax authorities to pay ¥3.5 billion in back taxes (including taxes, late fees, and penalties) due to consumption tax issues.

Whether viewed through Japanese laws and regulations or enforcement trends, Japan's imposition of consumption tax on overseas companies is an inevitable trend. Chinese companies expanding into Japan must pay attention to this and understand matters related to Japan's consumption tax. Regarding Japan's consumption tax, Kenting Law Firm invited Mr. Zong Zaijian from Japan's OHANA Tax Accountant Office to share insights. Below is a summary of key points from his presentation.

1. What type of tax is Japan's consumption tax?

Japan's consumption tax is similar to Value Added Tax (VAT), levied on goods and services sold or imported within Japan.

2. What are the latest requirements for consumption tax?

Conditions are becoming increasingly stringent:

(1) Tax liability arises if revenue exceeds 10 million yen during the base period.

Reference Period:

Individual business operators: The preceding two calendar years (e.g., 2023 reference period: January 1, 2021 – December 31, 2021);

Japanese corporations: The preceding two fiscal years (e.g., 2023 reference period: April 2021 – March 2022)

Special Period:

Businesses exceeding ¥10 million in revenue during the first half of the preceding year are also liable for consumption tax. (For 2023, the special period is January 1, 2022 - June 30, 2022)

Examples:

A. If revenue from January 1, 2022 to December 31, 2022 did not exceed 10 million yen, no consumption tax is required for the period from January 1, 2024 to December 31, 2024; However, if revenue from January 1, 2023, to June 30, 2023, exceeds 10 million yen, consumption tax must be paid from January 1, 2024, to December 31, 2024.

B. If revenue exceeds 10 million yen in both 2022 and 2023, consumption tax payment begins in 2024.

(2) Starting October 1, 2024, overseas companies with registered capital exceeding ¥10 million must pay consumption tax. [Based on registered capital, not actual paid-in capital].

3. Which in-game content (e.g., in-app purchases, one-time payments) may be subject to consumption tax?

For internet companies, user payments such as in-game purchases (items, skins, etc.) and purchases for games sold as a one-time purchase will be subject to tax.

4. If operating game business through a Japanese subsidiary, which entity bears the tax liability—the subsidiary or the parent company? How does the Japanese subsidiary file tax returns?

If establishing a corporate entity in Japan, the independent legal entity Japanese subsidiary files consumption tax returns as the taxpayer and must also pay corporate tax (similar to China's corporate income tax).

The Japanese subsidiary is required to file annually, choosing any month between January and March as its fiscal year-end. For example, if filing for the fiscal year ending January 2025, the reporting period would cover February 2024 to January 2025.

Overseas game companies typically close their fiscal year in December. The filing period in Japan is from January 1 to February 28 of the following year.

5. Does a non-resident company with no physical presence in Japan, solely selling mobile games via digital platforms, need to register as a consumption tax payer? What are the practical steps?

Appoint a designated tax representative (tax agent) in Japan, who will handle filing and tax payments through a certified tax accountant firm.

B2C: If taxable income is generated in Japan, register as a taxpayer. No tax number is required, and consumption tax exemption may apply (e.g., if revenue under ¥10 million in the previous two years).

6. Does a company without a Japanese entity need to appoint a Tax Representative? What is the relevant process?

Appoint a Tax Representative to handle filing and tax payments on behalf of the overseas company. In case of issues, contact the Tax Representative first.

Specific tax filing procedures: Self-filing is the primary method, typically involving submission of transaction records. Tax audits may occur if issues arise.

7. What are the penalties for underreporting or falsifying sales revenue (e.g., fine percentages, criminal liability)?

Criminal liability may apply if tax evasion exceeds ¥100 million.

Penalty rates:

(1) For regular filings:

- Under ¥500,000: 5%-15%

- Over ¥500,000: 15%-40%

(2) For concealed income:

- Penalty rate: 35%-40%